Introduction:

In the realm of personal finance, it’s fascinating how the size of our cash stash can influence our spending habits. From the way we allocate our daily expenses to the decisions we make about larger sums, our behaviour around money is often guided by subconscious processes.

In this blog post, we’ll explore the concept of mental accounting and its impact on our daily expenses. By understanding the psychology behind our financial decisions, we can take steps to manage our money more effectively and achieve our financial goals.

It’s intriguing how the amount of money we keep on hand can influence our spending behaviour. When we have a small amount readily available, we may be more inclined to spend it quickly on daily expenses. Conversely, when we have a larger amount, we might exhibit more caution and deliberation in our spending, recognizing that we have more to manage over time. This phenomenon underscores the psychological aspects of budgeting and financial management.

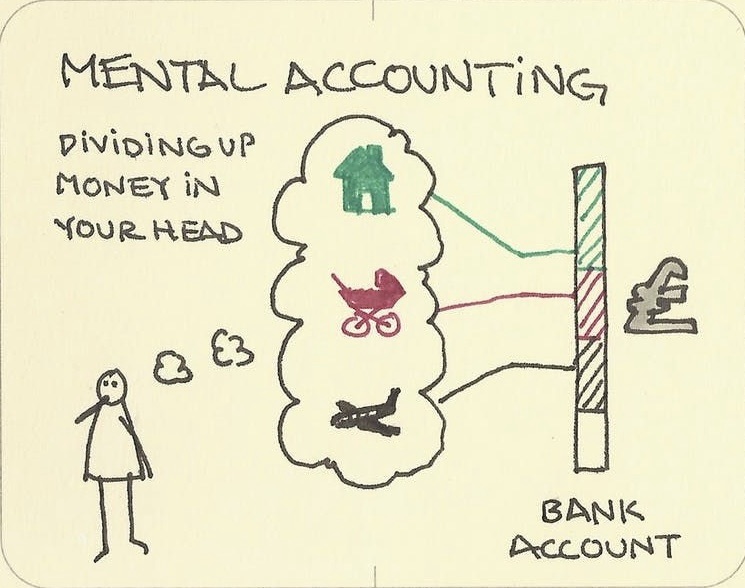

Mental accounting is the tendency of people to mentally categorize their money into different accounts or categories based on various factors such as the source of income, intended use, or emotional attachment. Keeping smaller amounts of money for daily expenditure creates a mental category for immediate spending, while larger amounts may be mentally categorized differently, leading to more cautious spending behaviour. Mental accounting can influence our financial decisions and behaviours in various ways.

Have you ever noticed that a small amount of cash set aside for daily spending seems to vanish quickly, while a larger sum appears to last longer? It’s not magic; it’s mental accounting at play!

This intriguing concept in behavioural economics delves into how we categorize and value money based on its origin (paycheck, bonus) or purpose (groceries, entertainment). Here’s why that little stash might be disappearing faster than expected:

Limited Perception, Limited Spending (Maybe): When you keep a smaller amount, you might perceive it as a separate “account” with less flexibility. This perception can lead to looser spending until the “account” is depleted. As Nobel laureate Richard Thaler explains in his book “Nudge,” we treat money differently depending on the mental bucket we’ve assigned it to.

Availability Bias: We tend to overestimate the likelihood of events based on how readily they come to mind (e.g., “winning the lottery”). A smaller amount might feel more accessible, subconsciously prompting you to spend more freely.

Research Supports it:

A study by Shafir et al. (1999) revealed that people spent more on a bowl perceived to contain less money, even if the total amount was identical to another bowl. Sound familiar?

Research by Heath et al. (1999) demonstrated that people are more likely to splurge on “found money” because it’s treated as a separate mental account from budgeted funds.

How Do We Outsmart Mental Accounting?

Framing Matters: Instead of viewing it as “all your spending money,” consider labelling the smaller amount as a “daily allowance.” Framing it as a limit can promote mindful spending.

Multiple Accounts: Divide a larger sum into smaller, labelled accounts (e.g., “groceries,” “transportation”) for enhanced control with flexibility.

Expense Tracking: Utilize a budgeting app or spreadsheet to monitor your spending patterns. Understanding where your money goes can facilitate adjustments to your strategy.

Remember, the best approach is the one that suits you best. Experiment and find a system that keeps your daily expenses in check without feeling overly restrictive. Ultimately, a little financial awareness can go a long way!

Conclusion:

The phenomenon of mental accounting sheds light on the intricate relationship between our perception of money and our spending behaviour. By recognizing the biases and tendencies that influence our financial decisions, we can adopt strategies to outsmart mental accounting and exercise greater control over our finances. Whether it’s framing our expenses differently, dividing our funds into multiple accounts, or tracking our spending patterns, the key lies in cultivating financial awareness and mindfulness. With the right approach, we can navigate our daily expenses more thoughtfully and pave the way towards a healthier financial future.

Note:-

Integrating Mental Accounting with Astrology and Spirituality

Some people may intertwine mental accounting with their astrological or spiritual beliefs as part of their financial management approach. For example, someone who follows astrology allocates specific funds for expenses based on astrological predictions or auspicious timings. Similarly, people with spiritual beliefs assign different monetary categories based on their spiritual practices or values, such as allocating funds for charitable giving or offerings.

In this way, mental accounting can intersect with astrological or spiritual beliefs to guide financial decisions and behaviours.

Explore more insights from Rise&Inspire

# The Job Market Trends and Challenges

Discover more from Rise & Inspire

Subscribe to get the latest posts sent to your email.

Never knew that. Thanks for indepth post. Money is a very positive energy and we should be mindful how we perceive it⭐

You’re welcome! Indeed, money can be a powerful force, and it’s important to have a healthy perspective on it. It’s not just about the tangible value it holds, but also the mindset and energy we attach to it. ⭐

Inspiring I must say 🥺😊

🤝